Closing Entry: What It Is and How to Record One

They arealso transparent with their internal trial balances in several keygovernment offices. Check out this articletalking about the seminars on the accounting cycle and thispublic pre-closing trial balance presented by the PhilippinesDepartment of Health. Opening entries, also known as initial entries, are made at the beginning of an accounting period. All opening entries should be recorded in the general ledger journal of the business and will represent the opening balance of accounts for the new period.

Closing Entry for Dividends (Capital Reduction)

The main purpose of these closing entries is to bring the temporary journal account balances to zero for the next accounting period, which keeps the accounts reconciled. To close revenue accounts, you first transfer their balances to the income summary account. Start by debiting each revenue account for its total balance, effectively reducing the balance to zero.

Closing Entries Accounting with Automation

Adjusting entries ensures that revenues and expenses are appropriately recognized in the correct accounting period. Once adjusting entries have been made, closing entries are used to reset temporary accounts. A sole proprietor or partnership often uses a separate drawings account to record withdrawals of cash by the owners.

Step #2: Close Expense Accounts

- For example, closing an income summary involves transferring its balance to retained earnings.

- In this example, the business will have made $10,000 in revenue over the accounting period.

- Closing entries are a fundamental part of accounting, essential for resetting temporary accounts and ensuring accurate financial records for the next period.

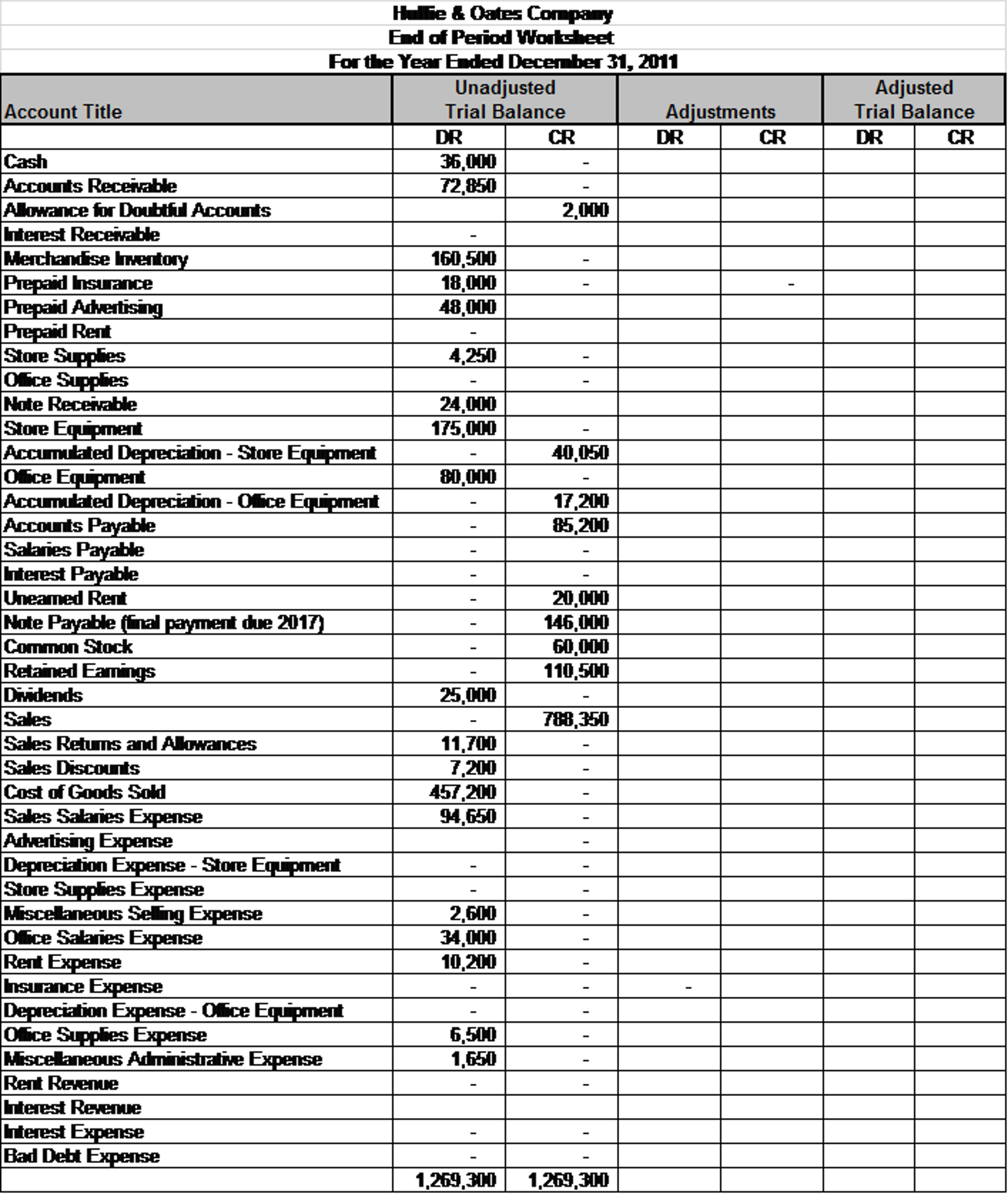

- The post-closing T-accounts will be transferred to thepost-closing trial balance, which is step 9 in the accountingcycle.

- Note that by doing this, it is already deducted from Retained Earnings (a capital account), hence will not require a closing entry.

When making closing entries, the revenue, expense, and dividend account balances are moved to the retained earnings permanent account. If you own a sole proprietorship, you have to close temporary accounts to the owner’s equity instead of retained earnings. The retained earnings account balance has now increased to 8,000, and forms part of the trial balance after the closing journal entries have been made. This trial balance gives the opening balances for the next accounting period, and contains only balance sheet accounts including the new balance on the retained earnings account as shown below. There may be a scenario where a business’s revenues are greater than its expenses.

Step 1: Transfer Revenue

There are various journals for example cash journal, sales journal, purchase journal etc., which allow users to record transactions and find out what caused changes in the existing balances. Closing entries are mainly used to determine the financial position of a company at the end of a specific accounting period. Closing entries, on the other hand, are entries that close temporary ledger accounts and transfer their balances to permanent accounts.

What are Closing Entries?

It is important to note that previous accounting period data should not be carried over into a new period, as it can greatly skew information and negatively impact businesses. Each period must use fresh accounts to begin recording transactions anew and start the process all over again. The permanent accounts in which balances are transferred accounting in 2040 depend upon the nature of business of the entity. For example, in the case of a company permanent accounts are retained earnings account, and in case of a firm or a sole proprietorship, owner’s capital account absorbs the balances of temporary accounts. The second entry requires expense accounts close to the Income Summary account.

To close that, we debit Service Revenue for the full amount and credit Income Summary for the same. Companies are required to close their books at the end of eachfiscal year so that they can prepare their annual financialstatements and tax returns. However, most companies prepare monthlyfinancial statements and close their books annually, so they have aclear picture of company performance during the year, and giveusers timely information to make decisions.

The closing entries are the last journal entries that get posted to the ledger. All expense accounts are then closed to the income summary account by crediting the expense accounts and debiting income summary. After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero. Permanent accounts track activities that extend beyond the current accounting period.

Notice that revenues, expenses, dividends, and income summaryall have zero balances. The post-closing T-accounts will be transferred to thepost-closing trial balance, which is step 9 in the accountingcycle. You might be asking yourself, “is the Income Summary accounteven necessary?

In step 1, we credited it for $9,850 and debited it in step 2 for $8,790. To close expenses, we simply credit the expense accounts and debit Income Summary. The fourth entry requires Dividends to close to the RetainedEarnings account. The income statementsummarizes your income, as does income summary.